Why Digital is an Advantage for Local Banking

It’s no secret that the world has gone digital. So much of everything we do each day happens online with the mobile devices that seem to be attached to our appendages. Mobile and desktop apps and online portals have changed the way we manage our lives, including our finances.

With the Millennial generation now the largest single population group in the workforce, the majority of spenders and financial decision-makers will soon be digital natives. They have grown up in the smartphone era and expect to be able to do just about everything digitally, including banking.

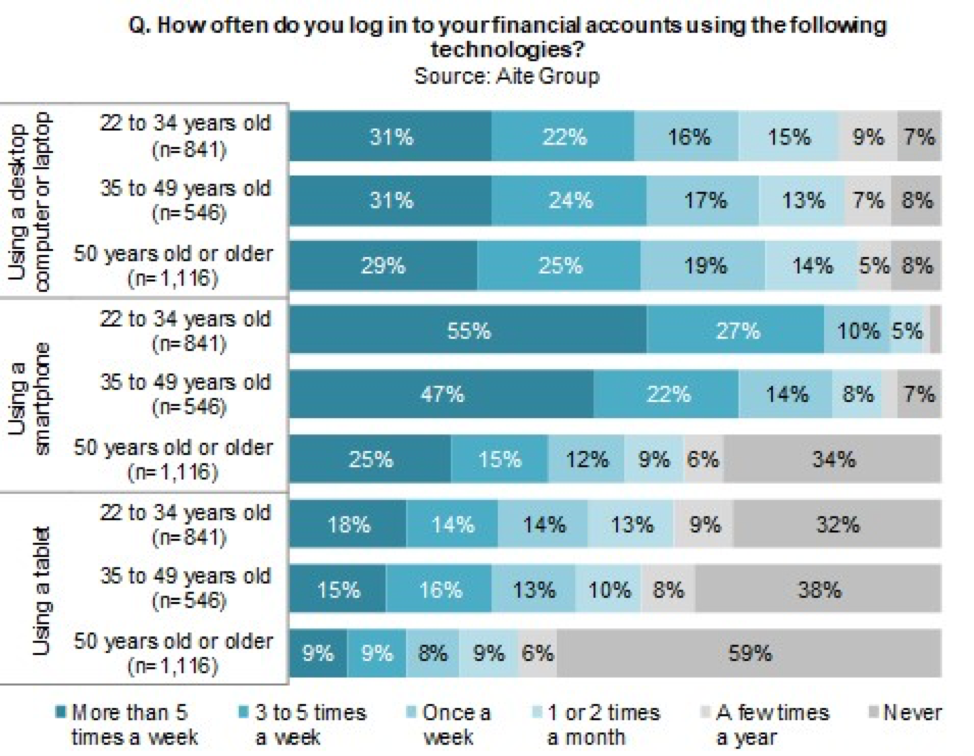

According to a recent report, 69% of Millennials use their laptops or PCs at least once a week to access bank accounts, but 92% do the same thing on their smartphones, and more than half engage in banking activities on their mobile devices more than five times a week.

Interestingly, Gen X is actually ahead of the Millennial generation in terms of laptop banking (82% at least once a week), and not far behind when it comes to smartphones (83% at least once per week and 47% more than five time a week).

The Milford Bank has always prided ourselves on the personal service we deliver and the community and human connections we are able to create. While on the surface it would appear that national banking brands would have an advantage with digital banking, we are happy to be provided the opportunity to build on our relationships we have had with our customers by offering a variety of digital products and services that can be correctly tailored to our customers’ needs and wants. Some of the advantages of this digital shift are:

Expanded customer base – Digital banking allows us to expand our customer bases. Because most people don’t need to visit branches very frequently, offering digital banking products can showcase our brand to new customers. Customers are comfortable doing most of their banking using digital tools, and are within a reasonable distance from a branch to be able to go when they need to.

Quality customer experience – The Milford Bank prides itself on delivering superior customer service. While it may seem digital banking could detract from that experience, it’s actually quite the opposite. Because customers expect to be able to do their banking online, giving them the tools to do it is part of a great experience.

Improved customer engagement – Digital tools create opportunities for increased engagement between The Milford Bank and its customers. That means that we now have more ways to let our customers know about the tools that are available for their banking needs – especially new ones, like partnering with P2P payment networks, and to emphasize the flexibility the combination of local and digital banking offers.

Perpetual availability – One of the great benefits of digital banking is its 24/7/365 availability. While offices are closed for holidays, the Internet stays open for business, which means you can access your accounts, pay bills, and send money to your kids in college any time at all – from anywhere.

The bottom line is banking is going digital, and it is important for The Milford Bank to give our customers a diverse variety of tools to choose how they want to bank. As banking competition has moved online, The Milford Bank cherishes the opportunity to blend the personalized experience a customer gets when they visit one of our offices with the ease and convenience of our digital product offerings. Customers like feeling that they matter and it is important for us to provide quality products and services regardless of whether it is in person or online.

{kind=link}