So You’re a First-Time Home Buyer, Here’s What You Need to Know

By Paul Mulligan

Buying a home is one of the biggest milestones in your life – right up there with marriage and starting a family. Being a homeowner has several benefits, including possibly lowering your monthly payments compared to renting and earning equity as your home value rises and you pay down your principal. The immediate benefit, of course, is the happiness and security of owning instead of being beholden to a landlord. As a homeowner, you have the ability to do what you like with pets, landscaping, renovations, and anything else that will make your house a home.

But, buying a home is also probably the biggest financial commitment you’ll make. There are many things to think about as you begin the process that can help make the process as enjoyable as it should be.

Here are several tips that can help make your first home purchase a positive experience.

Buy within your means – Many people tend to look at houses they can’t afford or that are too large. Do the math to determine how much you can realistically spend while still allowing you to meet your monthly budget needs, as well as continuing to save for retirement and other future needs – including home maintenance and repairs.

Understand all your costs – In addition to the basic monthly mortgage payments, be aware of all the other costs that may impact your budgeting. That includes property taxes and homeowners insurance, as well as mortgage and hazard insurances, depending on your financing need and location of the home. You should also expect an increase in your utility bills, including heating and HVAC maintenance contracts – especially if they were previously included in your rent payments.

Plan ahead – Don’t rush into a home purchase. Make sure you have all the information, have the financial resources to comfortably support the purchase, and are buying a home you will be happy in for many years. Try to avoid draining all your savings and make sure you still have an emergency fund to fall back on should the need arise. That’s particularly important as a homeowner so you don’t risk losing your house if you’re suddenly unable to make payments for a short period. In fact, it’s even better if you can continue to grow your savings, so you have the resources to make improvements.

Manage your credit – It’s always important to follow good spending and credit habits, but especially when you’re looking to buy your first home. Lenders will pull your credit reports, possibly several times, to make sure you are credit worthy and nothing has changed during the buying process. Make sure you pay your bills on time, and be cautious opening up any new lines of credit before your loan is approved.

The perfect home vs. the right home – It’s rare that you’ll find the absolute perfect home for all your current and future needs. Have a reasonable list of must-have features, and a second list of nice-to-haves. Look for a home that checks off the first set, and maybe some of the second (you can always make improvements to check off more items later). But don’t forget location. Your neighborhood can be as big a factor in your long-term happiness as the house itself. Do your homework and learn about the school system, commuting options and time, crime rates, tax rates, and other geographically dependent variables that may influence your decision.

Start the loan process early – As you start thinking about buying a house, don’t think you have to find the house first. In fact, you may be better off starting the loan process while you’re looking, or even before you start. Good houses can sell quickly, and once you find the house you love, you want to be able to move quickly. Being pre-qualified for a home loan may give you an advantage over other potential buyers, especially if the seller wants to move quickly.

Seek advice – Especially as a first-time buyer, you will have many questions of your own, and many more you don’t even think to ask. Contact one of our mortgage specialists, who can give help you find all of the information you need and help you throughout the process. Also ask about our first-time home buyer program, which offers:

Keeping these tips in mind will help you have an enjoyable home buying experience and avoid complications that could arise.

*The Milford Bank is an Equal Housing Lender

What Does the New FICO Scoring System Mean?

by Paul Mulligan, SVP, Retail Lending

When you apply for a loan, lenders have access to a variety of information they use to decide whether to give you a loan and at what terms. The most popular of those resources is your FICO score, a three-digit rating based on information in your credit reports, which helps lenders decide how likely to repay a loan, how much you can borrow, the length of you loan repayment period, and your interest rate.

While FICO scores give lenders a quick and consistent way to determine borrower worthiness, they also make sure you, the borrower, get a fair credit assessment and access to the funds you need. FICO has become the de facto industry standard for lenders.

This month, FICO has updated its scoring system for the first time since 2014, which could impact your scores. The new scoring places more emphasis on trend data in your credit report, looking at your credit utilization and payments over the past two years, as opposed to only current balances. For instance, new data might include whether you tend to pay off balances quickly, carry extended debt, or consolidate loans, as well as your credit management predictability.

The other major change reflects changes in credit reports. Tax liens, insurance-paid medical collections, and judgments are no longer part of credit reports, and healthcare defaults won’t appear on credit reports for at least six months.

At the end of the day, though, the real question is, how will the new scoring impact you?

The new scores will be less forgiving of risky credit behavior. That means, if you regularly run up your credit, don’t pay off balances consistently, carry too many credit cards, or consolidate debt into personal loans in order to free up your credit cards, you may see your score go down.

On the other hand, some spending habits that may have previously been viewed negatively may no longer hurt you. For instance, if you run up seasonal balances – such as during the holidays or summer vacations – and then pay them off, your score may not be negatively impacted because those are predictable one-time spikes, not regular habits.

Ultimately, what you need to keep in mind is the basics of good credit haven’t changed. Payment history (35%) and credit usage (30%) are still the two biggest components of your FICO score. If you follow good credit practices – pay your bills on time, keep balances below your credit limits, and don’t apply for too many new lines of credit (or too often) – you should have nothing to worry about. In fact, if you manage your credit well, the new scoring could actually improve your score.

If you’re concerned about your credit rating and want to work to improve your score, the sooner you start following good financial habits and budgeting, the faster you can see positive change. Of course, it’s not always easy, so if you need help or want advice on how to become more responsible with your spending, talk to our specialists. They can provide information on financial best practices, budgeting and saving tips, and improving your credit. On the other hand, if you have managed your credit responsibly, you probably don’t have anything to worry about. Just continue to follow smart banking habits.

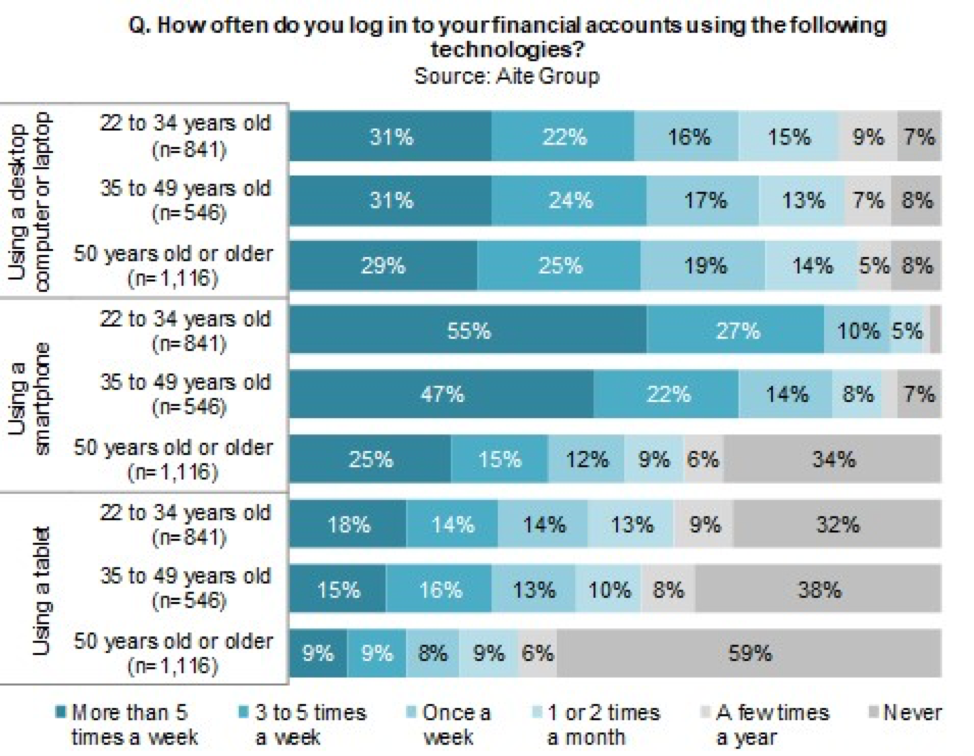

Why Digital is an Advantage for Local Banking

It’s no secret that the world has gone digital. So much of everything we do each day happens online with the mobile devices that seem to be attached to our appendages. Mobile and desktop apps and online portals have changed the way we manage our lives, including our finances.

With the Millennial generation now the largest single population group in the workforce, the majority of spenders and financial decision-makers will soon be digital natives. They have grown up in the smartphone era and expect to be able to do just about everything digitally, including banking.

According to a recent report, 69% of Millennials use their laptops or PCs at least once a week to access bank accounts, but 92% do the same thing on their smartphones, and more than half engage in banking activities on their mobile devices more than five times a week.

{kind=link}

Interestingly, Gen X is actually ahead of the Millennial generation in terms of laptop banking (82% at least once a week), and not far behind when it comes to smartphones (83% at least once per week and 47% more than five time a week).

The Milford Bank has always prided ourselves on the personal service we deliver and the community and human connections we are able to create. While on the surface it would appear that national banking brands would have an advantage with digital banking, we are happy to be provided the opportunity to build on our relationships we have had with our customers by offering a variety of digital products and services that can be correctly tailored to our customers’ needs and wants. Some of the advantages of this digital shift are:

Expanded customer base – Digital banking allows us to expand our customer bases. Because most people don’t need to visit branches very frequently, offering digital banking products can showcase our brand to new customers. Customers are comfortable doing most of their banking using digital tools, and are within a reasonable distance from a branch to be able to go when they need to.

Quality customer experience – The Milford Bank prides itself on delivering superior customer service. While it may seem digital banking could detract from that experience, it’s actually quite the opposite. Because customers expect to be able to do their banking online, giving them the tools to do it is part of a great experience.

Improved customer engagement – Digital tools create opportunities for increased engagement between The Milford Bank and its customers. That means that we now have more ways to let our customers know about the tools that are available for their banking needs – especially new ones, like partnering with P2P payment networks, and to emphasize the flexibility the combination of local and digital banking offers.

Perpetual availability – One of the great benefits of digital banking is its 24/7/365 availability. While offices are closed for holidays, the Internet stays open for business, which means you can access your accounts, pay bills, and send money to your kids in college any time at all – from anywhere.

The bottom line is banking is going digital, and it is important for The Milford Bank to give our customers a diverse variety of tools to choose how they want to bank. As banking competition has moved online, The Milford Bank cherishes the opportunity to blend the personalized experience a customer gets when they visit one of our offices with the ease and convenience of our digital product offerings. Customers like feeling that they matter and it is important for us to provide quality products and services regardless of whether it is in person or online.

Holiday Travelers Should Be Wary of New Payment Data Risk at Gas Stations

By David Wall,

Chief Information Officer

‘Tis the season… for joy and celebration and spending time with family and friends. It’s a time of year most people look forward to for many reasons, not the least of which is the traditions attached to the holiday period which, for many, includes travel. If you’re one of millions of people driving to visit your relatives this holiday season, there are plenty of things to deal with, from packing to wrapping presents, scheduling and, of course fighting holiday traffic.

This year, though, there’s something else to worry about. If you’re driving during the holidays, you’re going to eventually end up at a gas station, where you may be putting your payment cards at risk more than usual. Card skimmers have been around for a long time, but they can often be recognized by smart consumers and reported.

But, cyber criminals are getting more advanced and Visa has warned consumers of a new, growing risk at the pumps. A sophisticated hacking group has exploited vulnerabilities in gas station point-of-sale networks that allow them to install malware to intercept payment data from magnetic strip readers without any physical skimmer needed.

The problem is these attacks are undetectable to customers – until their accounts are used for fraudulent purchases or personal information is used in other ways, like opening new accounts. But, they are not entirely powerless. Because chip transactions have not been compromised through these breaches, customers should look for gas stations that have updated their technology and are using PIN or chip readers. Of course, good old cash is also a safe alternative.

Gas stations are facing an October 2020 deadline for installing chip readers at pumps, but until then, customers should be aware of the risk of using stripe readers.

This is yet another example of the continued threats to consumers’ financial and personal information, with new breaches reported almost daily that can cause significant hardship – or, at the very least, inconvenience – to victims. If you’ve suspect any of your financial information has been exposed in any way, please contact The Milford Bank right away so we can assist in resolving the issues. We also recommend subscribing to our Security E-Newsletter which offers informative articles and keeps you abreast of the latest threats.

Fraud and identity theft are the last thing anyone wants to have to deal with, least of all during the holidays. Staying informed and knowing how to reduce your exposure to risk can go a long way in keeping your accounts and data safe, and making sure you can enjoy the season.

What you need to know about using P2P payment apps

By Lynn Viesti Berube

One of the unique features about today’s app-centric society is there’s an app or just about everything, it seems. It’s great to be able to download apps and take care of so many things on your mobile devices. On the other hand, because these apps tend to be fairly targeted – most try to solve a single problem – they don’t always offer quite the level of flexibility or functionality users might want.

Take mobile payment apps, for instance, like Zelle or Venmo, which are becoming increasingly popular. They are designed to make exchanging funds between individuals easier using digital technology. But, they are not necessarily intended for all transactions. Both companies have been clear that their intended use is for payments between friends or other people who know and trust one another. For things like paying a share of a dinner bill, sending an entry fee for a fantasy sports league, or getting in on a group birthday gift, apps like these make transactions fast and simple. These are cases where one individual outlays funds for an activity, and others need to pay their share.

But, as with any digital transactions, there are risks that users should be aware of. Here are a few simple tips to keep your apps, accounts, and money safe while letting you enjoy the convenience of P2P payment apps.

Intended uses – Use the apps as they are intended. If an online retailer asks you to pay using a p2P app, you should be suspicious. Reputable online retailers should offer payment methods that don’t require immediate P2P transfers, such as credit cards, PayPal, and other means. If you’re paying for services, such as a snowplow service in the winter, using a P2P app, you may be using local residents not set up to receive credit card payments, and sending a check each time it snows can be a nuisance, so a P2P app might be the best option. At the very least, make sure you know who you’re paying, use only reputable providers, and make sure you’ve received the service before paying. Consider sending a check the first few times to make sure the relationship works out.

Identity – It’s easy to make a mistake when typing an email, phone, number or username. Double check whatever identifier you’re using to send money to someone. Once the money has been sent, it’s hard – often impossible – to get it back, so taking the extra time to get it right can reduce potential headaches.

Send a test – If you’re not certain you are sending to the right person, send a small amount as a test and confirm they received it before sending the full amount.

Security – Follow the same security principles as you would for any other application or website. Use the highest level of security they offer, including using a PIN or fingerprint ID for transactions. If the application offers two-factor authentication, be sure to use it. While this adds an additional step when using the app, it also adds an additional layer of protection that help keep you account secure, even if your credentials are compromised.

Deposits – Some apps place funds you’ve received into a mobile wallet until you manually transfer them into your bank account. This can sometimes take several days to process, so once you have approved the transfer, check to verify that it actually went through.

Fees – Some P2P payment platforms charge fees for certain kinds of transactions. Make sure you know what your app’s policies and fees are so you won’t be surprised and can account for fees when sending or receiving money.

Settings – Always check your app’s privacy and sharing settings. They may have default settings that make information available to others that want kept private.

Kids – Many parents want to give their children access to P2P payment apps to make it easier for them to participate in various activities. You probably don’t want to give them full access to your credit card or bank accounts, so take the trip to your local bank to see what options they might be able to offer, such as a prepaid debit card to link to your child’s app. If they are part of one of the payment platform networks, they likely are well versed on the best ways to let your kids use them. Of course, before anything, make sure your child’s device has security protocols enabled, and talk to them about potential security risks and how to avoid them.

Peer 2 Peer Payment Apps Give Consumers More Choice

By Celeste Lohrenz

As it has been with nearly every industry, digital technology is changing the way people bank. Online tools and mobile apps are making it easier for people to manage their finances, giving them modern options to replace traditional options. P2P (Peer To Peer) payment apps, for instance, have become highly popular as a means of exchanging funds between individuals.

While check payments are still very popular – even with Millennials, new P2P payment users are nearly evenly split between those younger than and older than 45.

It’s really about having options. If there one thing a digital economy has proven it is that people want convenience. They want to be able to transact using whatever methods are most convenient for them at the time. That may mean going to a local bank office to understand the differences between home equity loans and HELOCs. It may mean putting a check in the mail for a monthly car payment. It may mean going to an ATM to take out cash for dinner. It may mean putting a new TV on a store credit account because of a no-interest offer. Increasingly, though, it also means using P2P apps to settle with friends, relatives, colleagues, or others.

For instance, Zelle – a mobile payment platform whose parent company is actually owned by seven major banks – delivered $49 billion through 196 million transactions in Q3 2019 alone, a year-over-year increase of 58% in transaction value and 73% in transaction volume. The Milford Bank is happy to now offer Zelle to our customers as a further option to your banking experience.

There are many reasons P2P payment apps such as Zelle are growing, but convenience is at the top of the list. Zelle offers a simple alternative to get money to other users quickly – if both parties are signed up with Zelle for instance, funds may be available within minutes. Zelle is available on both Android and iOS platforms, making it easy to transfer money to split a dinner tab or utility bill, regardless of what mobile devices your friends use.

But, perhaps the biggest benefit Zelle offers is trust. The biggest reason consumers avoid mobile payment apps is lack of trust. In addition to being operated by a consortium of the biggest banks in the country, Zelle partners with other financial institutions so those banks can make Zelle transactions available through their own mobile apps and online resources – as opposed to having to use a third-party app. Sending or requesting money is as simple as logging into The Milford Bank’s mobile app or online account and choosing the person to send funds to using your mobile contact list or entering their phone number or email address.

Along with The Milford Bank, more than 600 financial institutions have signed up to be part of the Zelle Network, with more than 250 already online and processing transactions. In all, more users representing more than 5,500 banks have successfully completed Zelle transactions.

How are You Getting Rid of Your Old iPhones and Computers?

By Dave Wall

Every time Apple, Samsung, or any other electronic device manufacturer releases new products, the media tends to grab hold and saturate news feeds with the incredible advances these new product bring for consumer and business users. They’re not wrong of course – think about all the things we’re now able to do from smartphone in our hands. It’s an unprecedented level of convenience, efficiency, and productivity, and the hype helps generate sales momentum as these new products become available.

But, what is left out is what to do with your old devices when you replace them. Of course, some phones are recycled when they are exchanged for new ones at mobile carriers like Verizon and AT&T. But when you consider the third-party market for not only phones, but other devices like tablets, laptops, smart watches, and the many other products that permeate today’s digital lifestyles, it’s clear that there’s an awful lot of electronic waste being created.

The United States alone generated almost 12 million tons of e-waste in 2014 according to the EPA. The UN reported that 44.7 million tons of e-waste was generated globally in 2016, and the World Economic Forum reported that number had risen for 485 million tons in 2018. That makes it the fastest-growing waste stream in the world. Yet, only about 20% was recycled. So, where do the rest of these items end up? Certainly, many are likely collecting dust in homes and offices, but a large percentage ends up in landfills or incinerators, both of which are harmful to the environment.

E-recycling offers an effective way to get rid of old electronics safely, but how should you recycle your electronics? There are many local retailers that will recycle e-waste – some of them regardless of where they were purchased. And of course, mobile carriers often offer rebates for trade-in that can be applied towards the purchase of a new device.

If you keep an eye on your community events, you will also likely find e-recycling opportunities. The Milford Bank, for instance, will be holding two Shred & Recycle Days this year, making it easy for residents to get rid of their old electronics, as well as paper documents.

The first TMB Shred & Recycle Day will take place on Saturday, May 4, 2019, from 10:00am-1:00pm at the Post Road West branch (295 Boston Post Road, Milford, CT), and will include free e-recycling for anyone and free document shredding for customers (non-customers may still take advantage of the shredding service for a $5 donation to a local non-profit).

The second Shred & Recycle day will take place in the fall, after families have purchased new laptops and tablets for the new school year, on Saturday, October 12, 2019 (10am-12pm).

Recycling electronics and paper provides a constant stream of resources that have countless uses, helps reduce the amount of junk that piles up in landfills across the globe, and reduces the environmental impact of dumping. There are many materials that can be harvested from old electronics that can be re-used to manufacture new ones, including, gold, silver, palladium, and copper. The WEF values the value of materials that can be recovered through e-recycling at more than $62 billion. Apple says it was able to collect more than a ton of gold from recycled devices in 2015. That’s worth more than $40 million.

Take a look around your home. If you have old electronics lying around that haven’t been used for years – and most households do – take advantage of this community service provided by The Milford Bank to do some good for the environment and get rid of some old junk from your home in the process.